Cost basis is the number you subtract from a sale price to figure out the gain. For physical bullion, it is also the number that most often gets recorded wrong — split across receipts, blurred into a single “price paid” cell, or lost entirely on inherited pieces. This guide covers cost basis precious metals investors need to understand: what counts, which method the IRS allows on coins and bars, what records to keep, and how to reconstruct what’s missing.

For the broader portfolio-tracking case, see the broader portfolio-tracking guide; for the per-piece inventory step-by-step, see the step-by-step inventory guide.

This article is for informational and educational purposes only and is not tax advice. Specific situations — inheritances, gifts, IRAs, multi-state filings — belong with a qualified tax professional. The longer version of that disclaimer is at the bottom.

What “cost basis” means for precious metals

For physical precious metals, cost basis is the all-in dollar amount you paid to acquire a specific coin or bar — the spot price at purchase plus the premium over spot, plus any allocated shipping or acquisition costs. It is the figure subtracted from sale proceeds to compute gain or loss when the piece is eventually sold.

Cost basis is not current value. Current value moves with spot every minute; cost basis is fixed at the moment of purchase and stays put. Cost basis is also not melt value. Melt value is metal content multiplied by today’s spot — a pricing concept for what a coin would liquidate at.

Cost basis is the historical fact of what you actually paid, including the premium the dealer charged on top of the metal.

Why cost basis matters more for bullion than for stocks

Physical bullion is treated as a collectible under US tax law, and that classification carries three downstream rules that don’t apply to a typical stock holding.

First, long-term gains on physical bullion are subject to the collectibles rate — a federal cap of 28%, applied as the lesser of 28% or the seller’s ordinary marginal rate. It is a cap, not a flat tax: a filer in the 22% bracket pays roughly 22% on the gain; a filer in the 35% bracket pays 28%. The full mechanics are in the 28% collectibles-rate explainer.

Second, the short-term vs. long-term threshold is 365 days from purchase to sale, identical to the stock rule. The difference is the downstream treatment: short-term gains are taxed at ordinary income rates, long-term gains face the collectibles cap, and the holding period is calculated per piece — not per transaction or per product.

Third, like-kind exchange treatment under §1031 was removed for collectibles by the 2017 Tax Cuts and Jobs Act. There is no deferral available on a bullion-for-bullion trade. Every sale is a realized event for tax purposes, regardless of what the proceeds are reinvested into.

What goes into your cost basis (and what doesn’t)

The line between cost basis and non-cost basis is the line between acquisition cost and holding cost. Costs incurred to take ownership of the piece go in; costs incurred to keep owning it do not.

What counts

Cost basis is the all-in per-unit cost of taking delivery. The IRS guidance in Publication 551 (Basis of Assets) is broad — the basis of property is generally what you paid for it, including amounts paid to acquire and put it into service.

For physical bullion, that means the metal value plus the dealer’s premium plus any shipping and handling allocated to the piece, plus any sales tax or inbound courier fees you paid at acquisition.

- Spot price at the moment of purchase, per unit.

- Premium over spot, per unit, in dollars.

- Allocated shipping and handling on the inbound purchase.

- Sales tax paid at acquisition, where applicable by state.

- Inbound insurance, courier fees, and other costs paid to take delivery.

What doesn’t

Holding costs are real out-of-pocket dollars, but they are not part of the basis. The piece arrives in your possession at its all-in delivered price; everything spent after that point is a cost of ownership, not of acquisition. The most common misconception in this category is storage.

- Storage fees: Safe deposit box, depository, or vault costs paid after acquisition.

- Insurance premiums: Paid on the holding after the buy is complete.

- Appraisal fees mid-hold: Distinct from acquisition appraisals tied to the purchase.

- Outbound shipping and selling fees: These reduce sale proceeds rather than increase basis.

- Time-value-of-money or inflation adjustments: Not recognized by US tax law for collectibles.

The cost-basis methods the IRS allows on physical metals

When you own more than one of an identical product — three Gold Eagles, twenty Silver Maples — and sell some but not all of them, the basis question is which specific piece’s purchase price counts. The IRS recognizes three methods on collectibles, plus one that is notably not available.

| Method | How it picks the basis | Typical bull-market outcome | Available in GSL |

|---|---|---|---|

| Specific Identification | Seller designates the exact piece sold; that piece’s purchase price is the basis. | Lowest reported gain available because the seller can pick higher-cost pieces. | Yes — exclusive method. |

| FIFO (First In, First Out) | Oldest piece is treated as the one sold by default. | Higher reported gain (older pieces have lower basis); more long-term treatment. | No. |

| LIFO (Last In, First Out) | Newest piece is treated as the one sold by default. | Lower reported gain (recent pieces have higher basis); more short-term treatment. | No. |

| Average Cost | All identical pieces share one averaged basis. | Not applicable — method is not allowed for collectibles under US tax law. | No. |

Specific Identification

Specific Identification is the most precise method. The seller designates the exact piece being sold and that piece’s original purchase price becomes the cost basis on the sale. The IRS broadly accepts Spec ID for assets where individual items are distinguishable from each other — physical coins and bars meet that test by default, since each carries its own purchase date, dealer, and price record.

A worked example. Suppose you own two 1 oz American Gold Buffalos. Coin A was bought eighteen months ago at a cost basis of $3,800; Coin B was bought three months ago at $4,790. Spot is hypothetically $4,850 today, and you decide to sell one.

Designating Coin A produces a long-term gain of $1,050; designating Coin B produces a short-term gain of $60. Same physical sale, two different tax outcomes, and the IRS lets you choose — provided you can document which coin you sold.

First In, First Out (FIFO)

FIFO treats the oldest piece as the one sold by default. Many tax-software packages and brokerage systems use it because they cannot track individual units inside a fungible position; they pick a buy-by-date order and move on.

On collectibles in a bull market, FIFO produces higher reported gains because older pieces have a lower cost basis, and it tends to push more sales into long-term treatment because the oldest pieces are most often the ones past the 365-day threshold.

FIFO is allowed on bullion. It is not required. The IRS framework permits Spec ID alongside it, and Spec ID is almost always more advantageous on collectibles because the seller controls the basis applied to the sale.

Last In, First Out (LIFO)

LIFO treats the newest piece as the one sold by default. The effect in a bull market is the inverse of FIFO: recent pieces have higher cost basis closer to today’s spot, so reported gains are lower, but more sales land in short-term treatment because the newest pieces are most likely still under the one-year threshold.

LIFO shows up in certain inventory-accounting contexts. It is less common for individual filers and rarely the right choice when Spec ID is available.

Average Cost — not available for collectibles

Average Cost basis is allowed for mutual fund shares and, in some treatments, for cryptocurrency. It is not an option for physical precious metals or other collectibles under US tax law. If a tax software prompt offers Average Cost on a metals sale, the asset is being classified incorrectly — usually as a generic ETF rather than as a physical collectibles holding. Re-classify and re-method before filing.

Which method to choose

Specific Identification is the right answer for almost every physical bullion sale. It gives the seller control over which gain is realized, which holding-period treatment applies, and which dollar amount of basis the sale runs against. None of the three other methods offer that control.

The realistic reasons to choose FIFO are administrative rather than strategic: a tracking system that cannot identify individual pieces, or a position that has been treated as fungible from day one with no per-piece basis recorded. Both of those are recordkeeping problems rather than tax-rule choices.

Spec ID stops being available when the underlying records can no longer support “which exact coin was sold” — keeping per-piece records keeps the option open.

The IRS expects consistency on a return. Switching methods mid-filing is not a flexibility handed out lightly, and many tax software packages lock the method choice at the first sale of the year. Pick the method that fits the record-keeping in place; ideally, that is Spec ID, supported by item-level records on every piece.

Cost basis for inherited or gifted pieces

Two situations come up often enough to deserve their own treatment. The basis rules in both cases are governed by IRS Publication 551 and the underlying Internal Revenue Code sections noted below.

Inheritance (stepped-up basis)

Under IRC §1014, the cost basis on inherited property generally steps to the fair market value on the decedent’s date of death — regardless of what the original owner originally paid for the piece. A coin a parent bought in 1985 for $400 and passed on at $4,500 FMV arrives in the heir’s hands with a $4,500 basis.

The holding period is treated as long-term automatically, even if the heir sells the day after inheriting. Documenting FMV with a contemporaneous source matters: a written dealer appraisal, a documented historical spot reference for the relevant date, or a probate valuation all work. For the broader estate-side treatment, see the inherited collection guide.

Gifts (carryover basis)

Under IRC §1015, gifted property is more nuanced because the basis depends on whether the recipient eventually sells at a gain or a loss. For a gain calculation, the recipient inherits the donor’s original cost basis — the gift carries the donor’s purchase price across. For a loss calculation, the basis is the LOWER of the donor’s basis or the fair market value at the date of the gift.

The holding period also carries over from the donor for gain calculations, which means a long-held coin can be gifted and sold immediately at long-term rates. The practical implications are unpleasant to discover at filing time — track the donor’s original records when receiving a gift, not just the FMV at the date the gift changed hands.

What records to keep (and for how long)

The IRS does not specify a one-size-fits-all bullion recordkeeping standard. What they expect is reasonable, contemporaneous evidence sufficient to support the basis figure filed on a return. The general statute of limitations on an IRS return is three years; that extends to six years when basis is substantially understated.

A working rule of thumb is to keep cost-basis records for at least three years after the year the piece is sold and reported, and longer for higher-stakes pieces or pieces inherited at meaningful values.

The minimum record set per piece, especially on anything you might eventually sell:

- Dealer invoice or order confirmation: Showing price, date, dealer, and order reference.

- Bank or credit card statement: Corroborating the dollar amount and the purchase date.

- Spot price reference for the purchase date: Especially for backdated entries where an auto-fill is today’s spot.

- Premium-paid record: Dollar amount split out from total price, on every purchase.

- Shipping and handling allocation: Per-item, especially on multi-item orders.

- Inheritance documentation: Appraisal or dated valuation establishing FMV at the decedent’s date of death.

- Gift documentation: Donor’s original cost basis records, gift date, and FMV at gift date.

Reconstructing cost basis when records are missing

Realistically, most people have some receipts and not others. Pieces bought years ago at coin shows, inherited holdings with no paper trail, gifted coins with no donor records — none of those are reasons to file an undocumented zero basis, which almost certainly overstates gain.

The IRS accepts reasonable reconstruction based on contemporaneous evidence, and the reconstruction method itself becomes part of the record. Document what method was used and what source data supports each piece. The full procedural treatment lives in the step-by-step inventory guide.

- Pull bank or credit card statements covering the purchase date and back into spot and premium from the recorded dollar amount paid.

- Look up historical spot for the purchase date (Kitco historical chart, BullionByPost) and add a reasonable premium estimate for that product and that year — document both.

- For inherited pieces, document fair market value at the decedent’s date of death and use that as basis under §1014.

- For gifted pieces, request the donor’s original records or, if unavailable, document FMV at the date of the gift along with the basis treatment used.

How Gold Silver Ledger handles cost basis

Cost basis in Gold Silver Ledger is built into the data model rather than computed after the fact. Each of the rules above maps to a specific behavior of the Record Purchase form, the inventory item record, or the Annual Report.

Specific Identification by design

Every coin and every bar is its own inventory record. Buy ten American Silver Eagles in a single transaction, and the ledger creates ten separate items, each with its own purchase price, purchase date, and per-piece basis. When a sale is recorded, the user ticks the exact pieces, leaving your portfolio — not a quantity field, not a product-level pick.

The sold item’s locked basis becomes the cost basis row on the Annual Report. FIFO and LIFO are not offered as toggles because Specific Identification is the most precise method and the most often advantageous on collectibles, and the inventory model already supports it natively.

Spot at the moment of purchase, locked on the record

When a purchase is recorded, the live spot price at that moment is captured on the row and frozen. Live spot continues to drive the current-value side of the math — the dashboard’s portfolio value, the gain/loss on every held position — but it never moves the cost basis side.

For backdated purchases (an invoice from a 2019 buy, a stack of coin-show receipts from several years back), you can overrides the auto-filled current spot with the historical spot for the relevant date. The basis recorded then survives every spot move since.

Premium-over-spot as a first-class field

The Record Purchase form asks for premium per unit in dollars, not as a percentage of spot and not as part of a total-price field. Cost basis becomes melt plus premium structurally — no derived columns, no formula drift, no rounding artefact from a stale spot reference.

The single most common mistake on first entry is typing the total amount paid into the Premium per Unit field; the live Total Cost strip at the bottom of the form catches it because the total looks roughly twice the actual purchase.

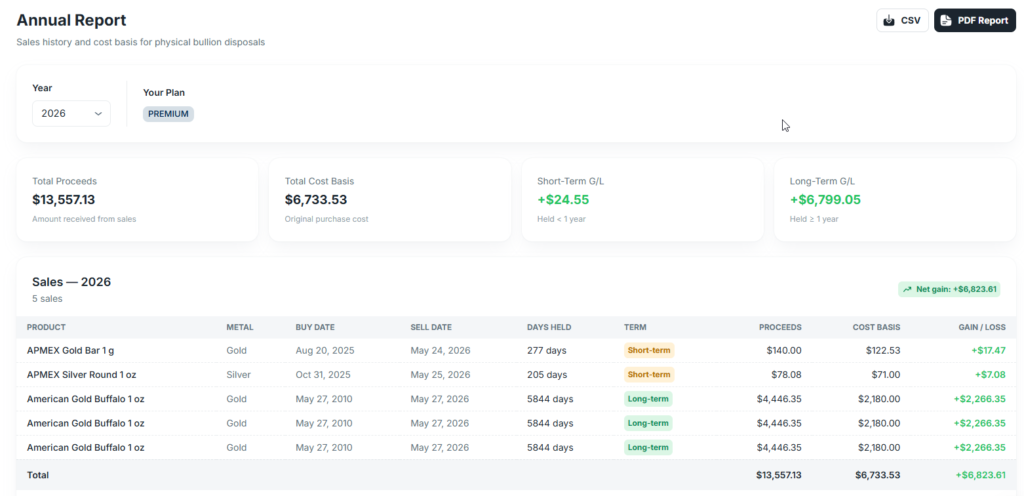

The Annual Report rolls it up

At tax time, every sold item appears on its own row of the Annual Report with the Cost Basis column already populated from the per-piece data locked at purchase. Short-Term and Long-Term G/L cards above the table split the year’s sales by the 365-day rule.

The Annual Report itself is Premium-only, but the per-piece cost-basis tracking that drives it runs on every plan, starting the moment a sale is recorded. The report stops at gain or loss — it does not compute tax owed, because the bracket math, state rules, NIIT exposure, and offset positions all sit outside the app.

Common cost-basis mistakes

Most cost-basis errors are recordkeeping habits rather than misunderstandings of tax law, and most of them are fixable before the next sale. The six below show up repeatedly enough to be worth naming.

- Recording the total price paid instead of splitting spot and premium — the single most common error on hand-built records.

- Letting tax software default to FIFO or apply Average Cost without classifying the asset as a collectible.

- Treating storage fees, post-acquisition insurance, or other holding costs as part of cost basis.

- Forgetting to allocate shipping across line items on a multi-item purchase.

- Recording today’s spot on a backdated purchase instead of the historical spot from the receipt date.

- Filing an undocumented zero basis on inherited pieces instead of researching FMV at the decedent’s date of death.