You sold a tube of Maple Leafs or a kilo bar at a long-term gain, and somewhere in the reading you have done about gold capital gains tax, the number 28% keeps surfacing. The headline rate looks worse than the long-term rate on stocks.

The article in one sentence: 28% is a cap on long-term collectibles gains, applied as the lesser of 28% or your ordinary marginal rate. For most filers, the cap never binds.

Below, we’ll cover when it does, what layers on top, and how the inputs the rate needs come together at filing time. The cost-basis and dealer-reporting sides have their own pieces in the full cost-basis guide and the 1099-B sibling article.

The headline rule, in one sentence

Under US federal tax law, long-term gains on physical precious metals are taxed at a federal rate capped at 28%, applied as the lesser of 28% or the seller’s ordinary marginal rate. Short-term gains follow ordinary-income treatment with no 28% cap.

“Long-term” here means held for more than one year between buy date and sell date. A position bought in June 2024 and sold in July 2025 is long-term; a position bought in June 2025 and sold in March 2026 is short-term.

The most-repeated mistake on this topic is treating 28% as a flat tax. It is not. The cap binds for some filers and is irrelevant for others. The next two sections explain why — first, the statutory hook that puts physical bullion in the collectibles bucket, then the cap mechanic that decides whether the rate actually applies to you.

Why physical bullion lands in “collectibles”

The capital-gains rate hook for bullion is IRC §1(h)(4)(A), which subjects “collectibles gain” to a maximum federal rate of 28%. The statutory definition of “collectible” sits in IRC §408(m), which lists works of art, antiques, gems, stamps, coins, and “any metal or gem.” Physical gold, silver, platinum, and palladium — coins, bars, rounds, junk silver — all sit inside that definition.

A separate piece of §408(m) carves out specific bullion coins (American Gold Eagles, American Silver Eagles, American Gold Buffalos, and several IRS-approved fineness standards) from the collectibles list for IRA-holding purposes only.

That carve-out lets those coins sit inside a self-directed IRA without tripping IRA-distribution rules. It doesn’t exempt them from the 28% capital-gains cap when held personally and sold. See the Gold IRA guide for the IRA side of that rule.

The Eagle in your safe and the Eagle in your IRA share a §408(m) line in the code, but the rules on each end are different. On personal holdings, every realized long-term gain on physical bullion — Eagles, Buffalos, generic rounds, all of it — sits under the 28% cap.

How the 28% cap actually works

Three pieces of the cap mechanic decide whether it binds: the lesser-of rule, the bracket band where the cap starts to matter, and the practical takeaway for most investors.

It is a cap, not a flat tax

Long-term collectibles gains are taxed at the lesser of 28% or your ordinary marginal rate under IRC §1(h)(4). A filer in the 12% bracket pays 12% on a long-term bullion gain, not 28%. A filer in the 22% bracket pays 22%. A filer in the 24% bracket pays 24%. The cap only starts to bind once the marginal rate would otherwise exceed 28%.

Which brackets the cap actually binds for

Under the current federal brackets, the cap binds for filers in the 32%, 35%, and 37% brackets — roughly the higher-income tier of US filers, with the exact dollar boundaries reset by the IRS for inflation each year. The IRS Tax Topic 409 page carries the current dollar thresholds for the 32% bracket and above.

Why this matters for the reader

Many reading this article land in the 22% or 24% bracket and will pay their bracket rate on a long-term gain. The 28% headline never touches their return. The reader who has to plan around the cap is a higher-income filer for whom 28% is materially worse than the 15% or 20% long-term rate that applies to stocks and most other capital assets.

Worked examples by bracket

Three illustrative scenarios — the numbers are made up to make the mechanic legible, not a calculation for any specific filer.

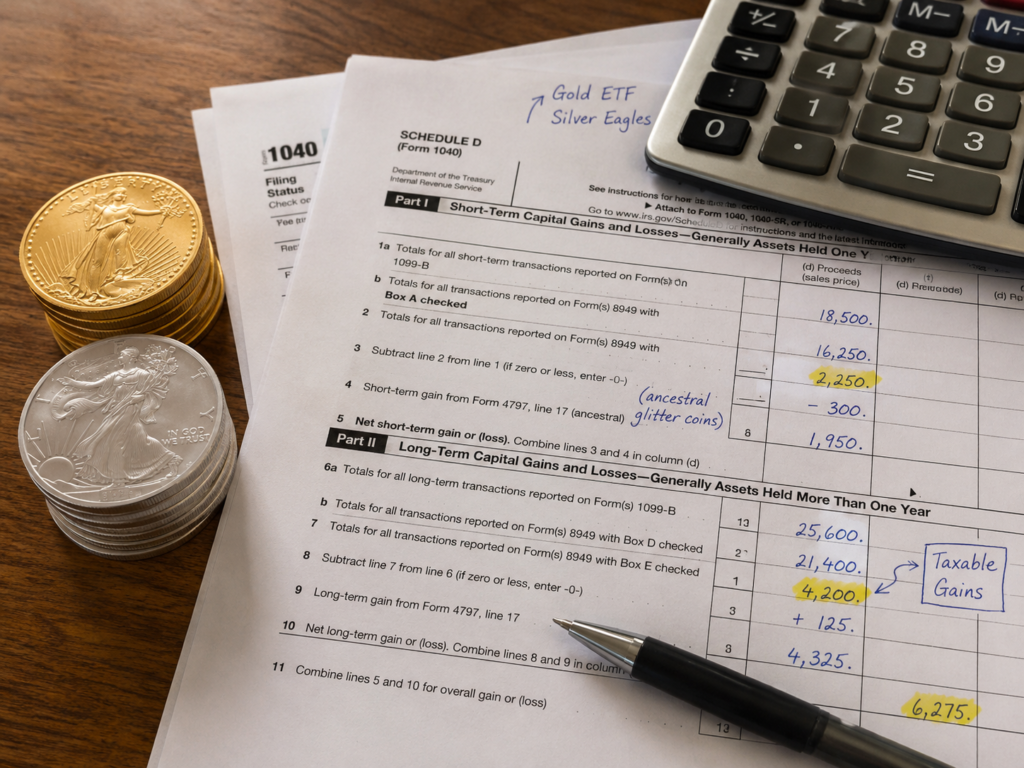

Suppose a 1 troy oz American Gold Buffalo bought at a cost basis of $3,800, sold eighteen months later for $4,850 — a $1,050 long-term gain. And a separate 1 oz coin bought and sold inside a year for a $400 short-term gain.

- 22% bracket, $1,050 long-term gain: Federal tax of ~$231 (gain × 22%). The 28% cap does not bind because the marginal rate is lower.

- 32% bracket, $1,050 long-term gain: Federal tax of ~$294 (gain × 28% cap). The cap binds because the marginal rate is higher than 28%.

- 22% bracket, $400 short-term gain: Federal tax of ~$88 (gain × 22%, the ordinary rate — no 28% cap on short-term gains).

Short-term vs. long-term — the 365-day line

Whether the 28% cap can apply to a sale depends on the holding period. More than one year between buy date and sell date is long-term. Held for 365 days or fewer counts as short-term and is taxed at ordinary income rates with no cap.

The calculation is calendar-day-based and runs per individual piece, which is exactly the per-piece basis logic the full cost-basis guide unpacks.

Two special cases. Inherited pieces are treated as long-term automatically under IRC §1223(9), regardless of how long the heir actually held the piece — a coin inherited last month and sold today still gets long-term treatment.

Gifted pieces inherit the donor’s holding period under IRC §1223(2) for gain calculations, so a coin gifted yesterday may already be long-term if the donor held it past the one-year mark. Both edge cases warrant a tax professional before filing.

What layers on top of the 28% rate

The federal collectibles rate is one piece of the all-in tax cost of a sale. Three other items can layer on top.

Net Investment Income Tax (NIIT)

Higher-income filers may owe an additional 3.8% Net Investment Income Tax on net investment income under IRC §1411, including collectibles gains. NIIT kicks in above modified adjusted gross income thresholds set by the IRS — current dollar boundaries are on the IRS NIIT page. For a high-income filer with the 28% cap binding, NIIT raises the effective federal rate to 31.8%.

State income tax

Most US states tax capital gains as ordinary income, meaning a state-resident filer may owe state tax on top of the federal collectibles rate at their state’s marginal rate.

A handful of states do not have a state income tax at all, and a few more carve out capital gains specifically. Multi-state filers — residency change during the year, income earned in more than one state — add another layer that this article does not try to model.

Alternative Minimum Tax (AMT) — usually not a factor

AMT runs in parallel with the regular tax system and has its own treatment of collectibles gain. Since the 2017 tax law, the AMT exemption is high enough that few individual filers owe AMT in any given year.

For many readers, this is a non-issue; the high-income filer who already wrangles AMT each year will know to mention the bullion sale to their tax pro before filing.

ETFs, mining stocks, and the 28% question

The collectibles classification follows the asset, not the underlying metal. That matters for readers who hold a mix of physical bullion and paper exposure — the rate on each piece is not the same.

Physical-bullion ETFs are usually collectibles too

Bullion-backed ETFs structured as grantor trusts — SPDR Gold Shares (GLD), iShares Silver Trust (SLV), iShares Gold Trust (IAU), Aberdeen Standard Physical Gold Shares (SGOL) — pass through the underlying physical metal as collectibles for capital-gains purposes.

Each share is treated as a proportional interest in the bullion the trust holds, so long-term gains face the same 28% cap that applies to physical coins. GLD trades through a brokerage account like any equity, but is taxed like the metal it represents.

Mining stocks and royalty companies are NOT collectibles

Shares of mining companies and gold or silver royalty companies are taxed as ordinary equity holdings. Long-term gains face the standard 15% or 20% long-term capital-gains rate, not the 28% cap.

The same applies to precious-metals mutual funds that hold mining stocks rather than physical metal. The asset is a corporate share, and the IRS rate follows the asset.

Losses, offsets, and prior-year carryforwards

Most filers with bullion sales have other capital activity in the same year — stock sales, real estate, crypto, other collectibles — and the netting between buckets affects the final number.

Long-term losses on collectibles offset long-term gains on collectibles first, then long-term gains on other capital assets. Short-term losses offset short-term gains first. A net capital loss against ordinary income is limited to $3,000 per year ($1,500 if married filing separately), with the unused portion carried forward.

A meaningful loss from a prior year may already be on the return waiting to offset the bullion gain you are about to realize. The mechanics get involved quickly when more than one bucket has both gains and losses; complex situations belong with a tax professional.

How Gold Silver Ledger surfaces the inputs the 28% rate needs

Gold Silver Ledger doesn’t compute tax owed. It doesn’t apply the 28% rate, run bracket math, or classify the asset as a collectible — those determinations belong to a tax advisor or to tax software with the asset class set correctly. What we do is surface the inputs the rate calculation needs.

Per-piece cost basis ready for the rate calculation

Each coin and each bar is recorded as its own item, with spot at purchase, premium per unit, and allocated shipping locked on the row at the moment of the buy. When a sale is recorded, you pick the specific pieces sold.

The per-row Cost Basis on the Annual Report comes straight from those captures — no batch averaging, no FIFO defaults, no formula drift. Whichever rate applies (the 28% cap or a lower marginal rate), it is applied to a gain figure that ties back to a specific receipt.

The Annual Report’s long-term / short-term split

At the top of the Annual Report, two cards split the year’s realized gain or loss into Short-Term G/L and Long-Term G/L. On the sales table below, every row carries its own Term chip set per item from the 365-day calculation.

A sale of five coins where four were bought 14 months ago and one was bought last week produces four long-term rows and one short-term row inside the same transaction. The split is the input the 28% cap depends on.

Holding-period clarity at filing time

For each sold item, Buy Date and Sell Date are on the row, Days Held is calculated, and Term is set. The tax advisor (or filer doing their own return) does not have to re-derive any of it; the columns on the report map directly onto the columns Form 8949 asks for.

The collectibles rate is then applied externally — either by the advisor or by tax software that classifies the asset correctly.

What the report deliberately doesn’t do

The report stops at gain or loss. Bracket math, the cap-or-marginal-rate decision, state tax, NIIT, AMT, offsets from other holdings, and prior-year carryforwards all sit outside the app — and would be confidently wrong if computed without seeing the rest of the return.

The Annual Report is on the Premium plan; per-piece cost-basis capture runs on every plan from the first sale recorded.

Common mistakes when applying the 28% rate

Five recurring errors. Each surface at least once a year on stacker forums; each is fixable before the next sale.

- Treating the 28% rate as a flat tax. It is a cap; the lesser-of rule applies, and most filers pay their marginal rate instead.

- Letting tax software apply the 15% or 20% long-term capital-gains rate to a bullion sale. The asset has to be classified as a collectible for the correct rate to apply.

- Forgetting that short-term gains follow ordinary income, with no 28% cap. A high-bracket filer can pay 35% on a short-term bullion gain.

- Assuming American Gold Eagles are tax-free because they are excluded from the §408(m) IRA collectibles list. The carve-out is about IRA eligibility, not capital-gains treatment.

- Ignoring state tax, NIIT, or carry-forward losses when estimating the all-in tax cost of a sale.

Frequently asked questions

What is the tax rate on selling gold?

Long-term gains on physical gold sold in the US are taxed at a federal rate capped at 28%, applied as the lesser of 28% or your ordinary marginal rate. Short-term gains (held one year or less) follow ordinary-income rates with no cap. State tax, the 3.8% Net Investment Income Tax for higher-income filers, and any prior-year capital loss carryforwards layer on top of the federal piece.

Are gold and silver taxed as collectibles?

Yes, physical gold, silver, platinum, and palladium are taxed as collectibles under IRC §408(m), with long-term gains subject to the 28% federal cap under IRC §1(h)(4). The classification covers coins, bars, rounds, and junk silver held personally. Bullion-backed ETFs structured as grantor trusts (GLD, SLV, IAU, SGOL) are also treated as collectibles. Mining stocks and royalty-company shares are not.

Is the 28% collectibles rate a flat tax?

No, the 28% collectibles rate is a cap on long-term gains, not a flat tax. The federal rate that applies to a long-term bullion gain is the lesser of 28% or your ordinary marginal rate. A filer in the 22% bracket pays 22% on the gain; a filer in the 24% bracket pays 24%. The cap only binds once the marginal rate would otherwise exceed 28%, which under current brackets means filers in the 32%, 35%, and 37% bands.

Do I pay 28% on gold ETFs like GLD?

Long-term gains on bullion-backed ETFs structured as grantor trusts — including GLD, SLV, IAU, and SGOL — are taxed under the same 28% collectibles cap as physical bullion, since each share is treated as a proportional interest in the metal the trust holds. The cap, again, is the lesser of 28% or your ordinary marginal rate. ETFs that hold mining stocks instead of physical metal are taxed as ordinary equity holdings.

How are short-term gains on gold and silver taxed?

Short-term gains on physical gold and silver — bullion held for one year or less — are taxed at your ordinary income rate, with no 28% cap. A filer in the 35% bracket pays 35% on a short-term bullion gain; a filer in the 22% bracket pays 22%. Short-term gains are reported on Form 8949 and the totals carry onto Schedule D, the same as long-term sales.

How long do I have to hold gold for long-term capital gains treatment?

Hold the piece for more than one year between buy date and sell date — 366 days or longer — to qualify for long-term capital-gains treatment. Anything 365 days or less is short-term. The calculation runs per individual piece, so a multi-piece sale can produce a mix of long-term and short-term rows in the same transaction. Inherited pieces qualify as long-term automatically.

Are American Gold Eagles tax-free?

American Gold Eagles are not tax-free. They are excluded from the §408(m) collectibles list for IRA-holding purposes only — that carve-out lets them sit inside a self-directed IRA without tripping distribution rules. On a personal holding sold outside an IRA, every realized gain on an Eagle is taxable, with long-term gains under the 28% collectibles cap. American Silver Eagles and American Gold Buffalos share the same treatment.

Does the 28% rate apply to mining stocks?

The 28% rate does not apply to mining stocks or royalty-company shares. Those are taxed as ordinary equity holdings, with long-term gains under the standard 15% or 20% long-term capital-gains rate. The same is true of precious-metals mutual funds that hold mining stocks rather than physical metal. The collectibles classification follows the asset, not the underlying commodity.

Estimate tax inputs for your sale in Gold Silver Ledger

The 28% cap operates on a few small inputs: which sales are long-term, which are short-term, and what the per-row gain is on each one. Gold Silver Ledger captures those inputs as the year goes — spot at purchase, premium per unit, and allocated shipping locked on every buy; specific pieces ticked at every sale; per-row Term and Cost Basis on the Annual Report at year-end.

This article is for informational and educational purposes only and does not constitute financial, investment, legal, or tax advice. The 28% rate is a federal cap; whether it binds depends on the filer’s overall tax picture, including marginal rate, state of residence, filing status, prior-year carryforwards, and NIIT exposure. For the parallel question of what triggers IRS reporting on a sale (separate from how the gain itself is taxed), see the IRS-reporting sibling article. Edge cases — inherited holdings sold, gifted pieces, IRA distributions, multi-state filers, AMT exposure — belong with a qualified tax professional.