Most homeowners policies cap theft of bullion and coins at around $200. That figure is not the personal property limit on the declarations page; it is a Special Limit of Liability buried in the policy form, and it lands on the bullion bucket regardless of what the collection is actually worth.

If you’re looking at insurance for gold and silver and assumed your existing homeowners coverage handled it, this guide walks through the gap and the four ways to close it: an increased limit endorsement, a scheduled rider, a specialty collectibles insurer, or off-site storage at a depository with its own master policy.

This article is for informational and educational purposes only and is not a substitute for an agent, broker, or policy review. The full disclaimer sits at the bottom of the page.

What your homeowners policy actually covers

A standard ISO HO-3 policy (the form behind most carrier-branded “special form” homeowners coverage in the US) does cover personal property against theft, fire, and a list of named perils. The Coverage C limit on the declarations page is the headline number, often set at 50% or more of the dwelling limit. That number is not the cap that applies to bullion.

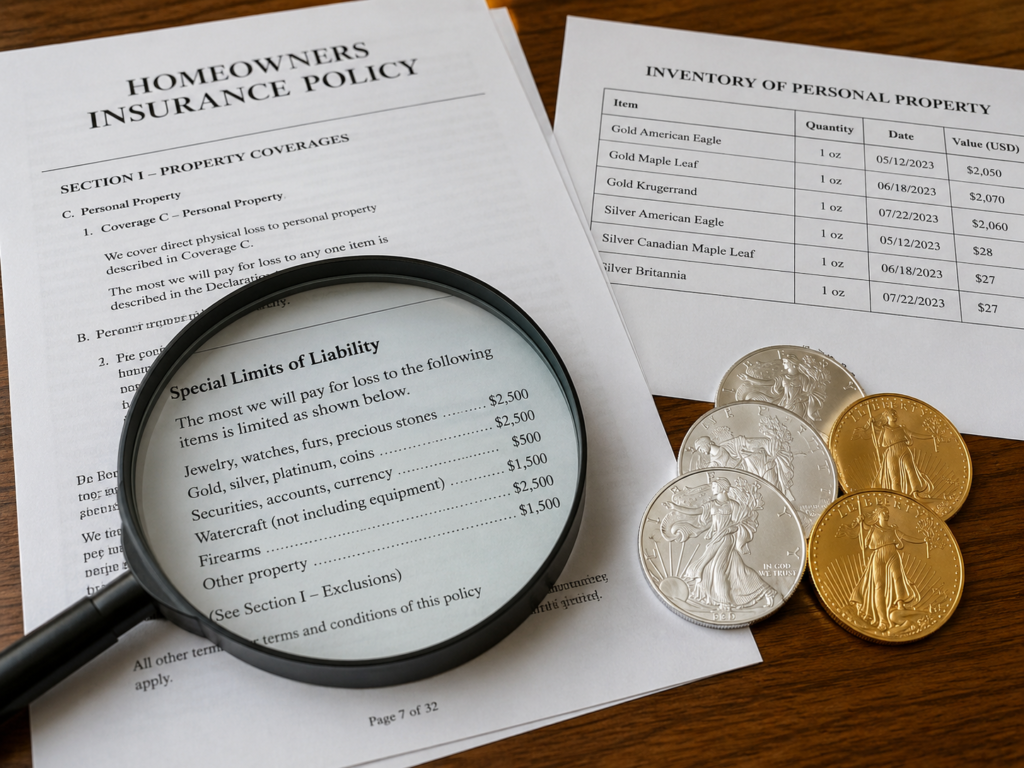

Inside the same form, a Special Limits of Liability section pulls a handful of categories out of the Coverage C bucket and caps them at much smaller numbers when the loss is theft. Money, bank notes, bullion, gold other than goldware, silver other than silverware, platinum other than platinumware, coins, and medals sit in the tightest of those caps.

The special limits that matter on a standard policy

Four sub-limits touch a precious metals inventory and the valuables typically stored alongside it. Each cap stands on its own; a single safe-contents theft can hit several at once, and the Coverage C personal-property limit on the declarations page is not what gets paid — each category is reconstructed against its own cap row by row.

Standard ISO HO-3 special limits of liability for theft (2022 form revision; carriers and state endorsements vary).

| Category | What’s in it | Typical theft sub-limit | Why it matters |

| Money, bullion, coins | Cash, bank notes, bullion, gold/silver/platinum other than ware, coins, medals | ~$200 total | Catches almost every bullion holding — Eagles, Maples, generic rounds, bars, junk silver |

| Jewelry, watches, stones | Jewelry, watches, precious and semi-precious stones | ~$1,500 total | Some carriers sit at $2,000–$2,500; numismatic coin grading rarely qualifies here |

| Silverware, goldware, platinumware | Flatware, tea sets, hollowware, trays, trophies made of or containing the metal | ~$2,500–$3,000 | Family silver lands here, not in the bullion bucket — a separate cap |

| Firearms | Firearms and related equipment | ~$3,000 | Often stored in the same safe — one loss can hit multiple caps at once |

Money, bank notes, bullion, and coins (~$200)

The tightest cap and the one that matters most. A safe holding $30,000 of bullion — Eagles, Buffalos, kilo bars, generic rounds, or junk silver — sits inside the same $200 limit on the unmodified form. Bullion is defined here by value from metal content, not by a purity threshold, so a .9167 fine Gold Eagle and a .9999 kilo bar both land in the bucket together.

Jewelry, watches, and precious stones (~$1,500)

A separate, slightly larger bucket. Some carriers and recent state-level endorsements sit at $2,000 or $2,500. People who hold graded numismatic coins occasionally argue for jewelry classification on individual pieces — that is a carrier-by-carrier judgment and not something to assume without written confirmation from the underwriter.

Silverware, goldware, and platinumware (~$2,500–$3,000)

Flatware, tea sets, hollowware, trays, and trophies made of or containing the metal sit in their own theft sub-limit. This bucket matters most for collectors who inherited family silver alongside coins and bars. The flatware piece and the bullion piece sit in different buckets on the same policy, even though both are silver.

Firearms and related equipment (~$3,000)

Out of category but worth noting because firearms are commonly stored alongside metals. The point is structural: a single safe-contents theft can hit two or three of these caps at once, and the agent reconstructs the loss against each cap separately rather than against the Coverage C headline.

Four paths to closing the bullion sub-limit gap

Four paths get a collection covered beyond the $200 cap. They are paths, not steps — the right one depends on collection size, the mix of pieces, and how much documentation you are willing to maintain. Most people end up with a layered approach as their holdings grows.

Four ways to cover a precious metals inventory above the homeowners sub-limit.

| Path | Documentation required | Coverage type | Best fit |

| Increased-limit endorsement | Stated value; usually no per-item list | Blanket; replacement-cost or stated-value | Collections under ~$10,000 with no high-value individual pieces |

| Scheduled personal property rider | Per-item inventory + appraisal above carrier threshold | Agreed value per piece; broader peril list | Collections with named high-value pieces |

| Specialty collectibles insurer | Inventory; appraisal often waived under carrier thresholds | Blanket, scheduled, or layered | Collections above ~$25,000, or collectors wanting a numismatic-aware underwriter |

| Off-site depository storage | Storage agreement; depository’s own inventory record | All-risk under depository master policy | People comfortable holding metal off-site with monthly fees |

Path 1: Increased-limit endorsement (blanket)

A blanket bump on the bullion category, sometimes called an increased-limit endorsement or a Coverage C enhancement. It raises the bucket-wide cap (for example, from $200 to $5,000 or $10,000) without itemizing pieces. Documentation is light and the premium is modest.

The trade-off: per-item sub-limits inside the blanket may still apply, agreed-value coverage is rarely available, and a single high-value piece may not net the full amount you expected.

Path 2: Scheduled personal property endorsement (rider)

The named-piece path. A scheduled personal property endorsement (also called a personal articles floater or valuables rider) lists each item with a stated value. The insurer agrees to pay the stated value on a total loss, often with no deductible and a broader peril list — including “mysterious disappearance,” which the unscheduled policy excludes. The trade-off is documentation: per-item inventory, professional appraisal above the carrier’s threshold (commonly $5,000), and policy updates whenever the collection changes materially.

Path 3: Specialty collectibles insurer (standalone policy)

A standalone policy from a carrier that writes collectibles as a primary product. Names you will see most often: Hugh Wood Inc. (the long-standing partner of the American Numismatic Association, now part of Risk Strategies), Collectibles Insurance Services (CIS / Collectinsure), American Collectors Insurance, and the high-net-worth desks at Chubb and AXA XL. These underwriters know the asset class, write blanket or scheduled coverage on the same policy, and often waive appraisals for items under a per-piece threshold. For collections above roughly $25,000, a specialty policy is usually the cleanest fit.

Path 4: Off-site storage with the depository’s insurance

Moves the coverage problem off the homeowners’ policy entirely. Allocated storage at a regulated depository (Brink’s, Loomis, IDS of Delaware, the Texas Bullion Depository) typically includes all-risk insurance under the depository’s master policy, with stated coverage limits on the storage agreement.

The trade-offs are monthly storage fees, metal you do not physically hold, and the fact that insurance attaches to metal at the depository — transit is a separate question. The full mechanics of depository vs. safe deposit box storage live in a dedicated guide.

What every insurer asks for (the documentation step)

Whichever of the four paths you pick, the insurer asks for the same five categories of documentation before it writes meaningful coverage. This is the step competitor articles skip and the one that gates everything else — the inventory is the precondition for the schedule, the appraisal, and the carrier’s price quote.

Start with the inventory itself. A per-piece list with product name, metal, form, fine weight, and acquisition date. Underwriters will not write meaningful coverage against a summary number (“about $40,000 in silver”); they want the file. Send a CSV or PDF the agent can attach to the policy record, then re-send a refreshed version each time the collection changes materially.

Next come the purchase records. Date of purchase, dealer, price paid, premium over spot price at the time, and shipping or other costs that built the basis — together these establish the replacement-value provenance the insurer validates against.

Photographs of higher-value pieces follow, along with an independent appraisal where the carrier requires one (commonly USPAP Standards 7 and 8, performed by an American Numismatic Association-credentialed appraiser for items above the carrier’s threshold). Storage and security at the residence round out the underwriting file.

How Gold Silver Ledger keeps your insurance file current

Insurers ask for an inventory and the records behind it. We built Gold Silver Ledger to keep both current automatically, so the file you send to an agent at scheduling, or re-send at renewal, is a one-click export rather than a weekend rebuild.

A per-piece inventory the underwriter can read

Each coin and each bar is its own row, with product, metal, form, fine weight, and purchase date. The Holdings page renders the same inventory three ways — grouped by metal and product, flat and sortable, or as a wall of product photos — so you can match whichever view the agent’s intake form expects.

Optional per-item labels (Nickname, Reference, mint year) carry serial numbers or personal SKUs into the search index where the carrier asks for them.

Purchase records that establish basis and provenance

Every Record Purchase entry captures the spot price at the moment of the buy, the premium paid per unit, the dealer, and any shipping allocated to the line. Those four fields are exactly the provenance an underwriter validates against when pricing a schedule or a blanket bump.

Because each capture is locked at the moment of the buy rather than reconstructed years later, the file holds together regardless of how much the spot price has moved since the original purchase.

One-document export the agent can drop into the file

The Annual Report exports a per-row layout — Product, Buy Date, Days Held, Cost Basis, Current Value — with CSV and PDF options. Most agents take the PDF directly; some carriers prefer the CSV for import. Either way, the export is a single attachment you can hand off at scheduling and re-pull at renewal as the collection changes.

How much coverage costs, and what changes it

Premium ranges are wide. As a rough guide, blanket increased-limit endorsements run a few dollars per $1,000 of coverage per year; scheduled riders cost more (often $5–$15 per $1,000) but include agreed value and a broader peril list; specialty collectibles policies vary by carrier but commonly land between the two. Every number here is illustrative — a quote depends on collection value, perils requested, residential security, claims history, and the state you live in.

Several carriers require a minimum security level for higher coverage tiers: a monitored alarm system, a fire-rated residential safe of a specified TL or RSC rating, or both. The requirement varies carrier by carrier, and a quote is the cleanest way to find out what your setup actually qualifies for.

Common mistakes when insuring precious metals

Five recurring mistakes show up at claim time. Each is fixable before the next renewal.

“My homeowners policy covers it“

Almost never beyond the ~$200 sub-limit. The personal-property number on the declarations page is not the cap that applies to bullion and coins — the special limit is, and it is much smaller.

Insuring a summary number instead of a schedule

Telling the agent “about $40,000 in silver” may get a blanket bump approved, but at claim time the carrier pays against documented items, not against estimates.

Skipping the appraisal on a high-value piece

Carriers commonly require an independent appraisal for any single item above $5,000. Without it, the rider may schedule the piece at a value lower than you expected, or exclude it entirely.

Forgetting transit and off-premises coverage

A standard scheduled rider covers the item at the residence; coverage for shipping, coin shows, exhibitions, or temporary off-premises storage is usually a separate endorsement that has to be requested.

Not updating the schedule when the collection changes

A rider written two years ago against $30,000 of holdings does not cover the $20,000 added since. Schedules require regular updates — renewal is the natural moment, but mid-term endorsements are usually allowed.

Frequently asked questions

Does homeowners insurance cover gold and silver?

A standard homeowners policy covers gold and silver only up to a Special Limit of Liability — typically around $200 for theft of bullion, coins, and money under the 2022 ISO HO-3 form. Fire, flood (if separately insured), and other named perils may apply against the full personal-property limit, but theft, which is the most likely loss for a precious-metals stack, runs against the sub-limit. Closing that gap requires an increased-limit endorsement, a scheduled rider, or a specialty collectibles policy.

How much does it cost to insure a coin collection?

Coin and bullion coverage typically runs between $0.50 and $1.50 per $100 of insured value per year on a scheduled rider, with specialty collectibles policies often falling in a similar range. Blanket endorsements on a homeowners policy are usually cheaper per dollar of coverage but cap out at lower limits and carry fewer perils. A $25,000 schedule may cost $125–$350 per year depending on the carrier, the perils requested, residential security, and your state.

Do I need an appraisal to insure my gold and silver?

Most carriers waive the appraisal requirement for individual pieces under a per-item threshold — commonly $5,000 — but require a professional appraisal for anything above it. Specialty insurers familiar with bullion will sometimes accept a dealer purchase receipt and a fine-weight calculation in lieu of a formal appraisal on standard bullion products. Numismatic pieces, graded coins, and rare items almost always require a USPAP-compliant appraisal from an American Numismatic Association-credentialed appraiser.

Who is the best insurer for a coin or bullion collection?

There is no single best insurer; the right carrier depends on collection size, mix, and storage location. For named numismatic collections, Hugh Wood Inc. (the ANA’s long-standing insurance partner, now part of Risk Strategies) is a common starting point. Collectibles Insurance Services (CIS) and American Collectors Insurance write standalone collectibles policies with flexible blanket-plus-scheduled structures. Chubb and AXA XL serve high-net-worth collections through their personal-lines desks. Most stackers compare quotes from two or three before binding.

Will my insurer cover coins stored in a safe deposit box?

A standard homeowners policy provides limited off-premises coverage for personal property, but the same Special Limits of Liability apply — so the bullion cap follows the metal into the safe deposit box. Bank safe deposit boxes themselves are not federally insured by the FDIC, and the bank’s own coverage typically excludes coins and bullion. A scheduled rider or a specialty policy with off-premises coverage is the usual way to cover safe-deposit-stored metal explicitly.

What documentation does an insurer ask for on a precious metals rider?

Insurers commonly ask for five things: a per-item inventory with product, metal, weight, and acquisition date; purchase records showing date, dealer, and price paid; photographs of higher-value pieces; an independent appraisal for items above the carrier’s appraisal threshold; and a description of where and how the metal is stored at the residence. Standardizing the inventory upfront makes the renewal cycle far easier — every subsequent schedule update reuses the same record structure.

Build the insurance-ready inventory in Gold Silver Ledger

Coverage starts with an inventory the underwriter can actually read. Gold Silver Ledger keeps a per-piece record of what you own — product, metal, fine weight, purchase date, what you paid, what you paid above spot — with search, filter, and three Holdings views to match whichever intake form your agent uses.

The Annual Report exports a single PDF or CSV the agent attaches to the policy file at scheduling, and again at renewal as the collection changes.

This article is for informational and educational purposes only and does not constitute insurance, legal, or financial advice. Sub-limit dollar amounts, peril definitions, and endorsement availability vary by carrier and by state, and ISO form revisions are not adopted simultaneously across every jurisdiction. Confirm coverage in writing with the carrier before relying on any framing here.

For tax treatment of a sale, the capital-gains explainer and the IRS-reporting sibling article cover the federal rate and the third-party reporting forms separately. Edge cases — inherited collections, IRA-held metals, multi-state residences, or any single item above $25,000 — belong with a qualified broker and a tax professional.